Outbound Domestic Loaded Rail Container Volume Surges, Signaling Major Shift in U.S. Freight Dynamics

The United States freight market is witnessing an unprecedented surge in outbound domestic loaded rail container volumes, with June 2026 data revealing a nearly 13% annual growth rate. This robust expansion is not a fleeting anomaly but rather the culmination of a steady build-up since spring, pushing volumes well ahead of the same period in every year dating back to 2020. This sustained momentum suggests a significant structural shift within the nation’s supply chain, as shippers increasingly turn to intermodal solutions for their logistical needs, driven primarily by compelling cost advantages over traditional truckload services.

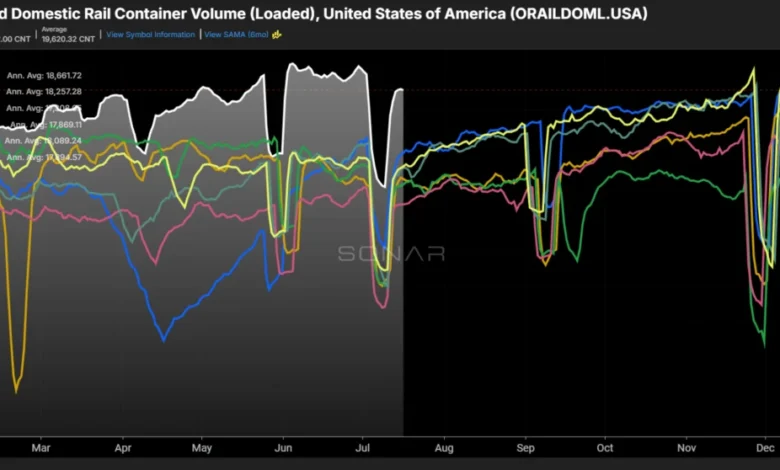

The Unfolding Intermodal Phenomenon: Data Speaks Volumes

According to FreightWaves’ SONAR data, which tracks the pulse of the freight markets, domestic loaded rail container volumes (specifically 48’ and 53’ units) have maintained peak-level performance throughout June. This summer surge is particularly noteworthy as it has already surpassed the volumes typically observed during the fall peak season of the previous year. Traditionally, domestic intermodal demand sees its highest activity in the autumn months, when retailers actively replenish inventories in anticipation of the crucial holiday shopping period. The current trend, therefore, represents a departure from established seasonal patterns, indicating a more fundamental change in freight procurement strategies.

It is crucial to differentiate these domestic intermodal movements from their international counterparts, which involve 20’ and 40’ containers directly tied to import and export demand. Domestic intermodal primarily competes with transcontinental truckload shipping, offering a multimodal alternative that leverages the efficiency of rail for long-haul segments combined with truck drayage for first and last-mile delivery. While historically favored for its cost-effectiveness over extended distances, rising truckload costs and capacity constraints, particularly on the East Coast, have broadened intermodal’s competitive appeal, enabling it to penetrate even shorter haul lanes.

Analysis of annual growth rates for the seven-day period ending July 16, 2026, depicted in a detailed tree map from SONAR, underscores the widespread nature of this intermodal boom. The data illustrates a remarkably even distribution of demand growth across various regions of the U.S., signaling that the shift is not localized but rather a national trend. This broad-based adoption further solidifies the argument that the current strength in intermodal is a systemic response to prevailing market conditions rather than isolated incidents of demand.

Industry Leaders Confirm the Shift: J.B. Hunt’s Record Performance

The observed strength in domestic intermodal volumes is unequivocally supported by recent corporate earnings reports from key industry players. J.B. Hunt Transport Services, the Lowell, Arkansas-based intermodal and dedicated freight giant, recently reported second-quarter 2026 results that significantly exceeded Wall Street estimates. The company’s intermodal volumes hit an all-time record, growing by an impressive 10% year-over-year. This performance notably outpaced the 8% year-over-year growth recorded across all Class I railroads and was well ahead of the 5% year-over-year increase in North American container volumes overall.

Darren Field, President of Intermodal at J.B. Hunt, highlighted the magnitude of this shift, stating that conversion activity from truck to rail is occurring at levels not witnessed in over a decade. This executive insight provides a critical qualitative dimension to the quantitative data, confirming that shippers are actively redirecting freight from road to rail on an unprecedented scale.

The timing of this surge is particularly striking. Typically, the intermodal bid season, where carriers and shippers negotiate rates for the upcoming year, does not formally commence until October. The traditional catalysts for such conversions—primarily climbing truckload rates and rising diesel prices—were not prominently present when the current bid season began last fall. This suggests that shippers are proactively engaging in intermodal conversions much earlier than usual, indicating a strategic, rather than purely reactive, decision-making process. The SONAR data corroborates this, showing that growth has been consistently distributed across the calendar year rather than concentrated within a narrow pre-bid window. This proactive stance by shippers points to a longer-term commitment to intermodal, driven by factors beyond immediate spot market fluctuations.

The Economic Imperative: Cost as the Primary Driver

At the heart of this dramatic shift lies the compelling economic advantage offered by domestic intermodal. FreightWaves’ SONAR Intermodal Contract Savings Index currently reveals that domestic intermodal is approximately 30% cheaper than truckload on a contract basis. This substantial discount far exceeds the 10% to 15% margin that J.B. Hunt typically cites as necessary to incentivize freight conversion from road to rail. Such a significant cost differential makes intermodal an irresistible option for shippers grappling with persistent inflationary pressures and the need to optimize their supply chain expenditures.

The broader truckload market environment further amplifies intermodal’s appeal. For several months leading up to June 2026, truckload rejection rates and spot rates have remained elevated. This indicates a constrained trucking capacity and higher operational costs for shippers relying solely on over-the-road transport. The confluence of a tight truckload market and competitive intermodal pricing creates a powerful incentive for businesses to re-evaluate their transportation modes. Truckload capacity has been impacted by various factors, including an ongoing driver shortage, increased regulatory compliance costs, and fluctuating fuel prices, all contributing to higher operating expenses for trucking companies, which are then passed on to shippers.

The efficiency gains inherent in intermodal also contribute to its cost-effectiveness. By leveraging the fuel efficiency of rail for the bulk of the journey, intermodal can offer a more economical and often more environmentally friendly solution for long-haul freight. This is particularly relevant as companies increasingly focus on sustainability targets. J.B. Hunt’s intermodal container fleet, a critical asset for the company, achieved over 90% utilization in the second quarter of 2026—a first in several quarters. This high utilization rate underscores the intense demand for intermodal services and the effective deployment of available assets to meet that demand.

Geographic Hotspots and Untapped Potential

While the growth in domestic intermodal demand is broad-based across the U.S., specific regions are showing even more pronounced shifts. Management at J.B. Hunt has identified "massive opportunities" for further conversion, particularly in the Eastern United States. In this region, intermodal services are proving to be more directly competitive with truckload rates, and J.B. Hunt’s intermodal volumes saw a significant 16% year-over-year increase in the second quarter, representing an impressive 31% growth on a two-year stacked basis.

The East Coast’s dense population centers, extensive manufacturing base, and intricate distribution networks make it a prime candidate for intermodal expansion. Historically, shorter average hauls in the East sometimes made truckload more competitive. However, with the current landscape of elevated truckload costs and capacity limitations, intermodal’s value proposition has strengthened, even for lanes that might have previously been considered marginal. The investment by Class I railroads like CSX and Norfolk Southern in expanding their intermodal networks and terminals in the East has also played a crucial role in enabling this growth, providing the necessary infrastructure to support increased volumes.

Operational Headwinds and the Question of Sustainability

Despite the overwhelmingly positive demand signals, the intermodal sector faces its own set of operational challenges that could test the sustainability of this rapid conversion. While rail service is a critical component, current data indicates that rail speeds have been slowing. Interestingly, this deceleration has not been sufficient to dampen shipper demand, strongly suggesting that the significant price advantage is currently outweighing concerns about transit time. This highlights the acute focus on cost reduction within supply chains.

The primary risks to the intermodal sector do not necessarily lie within the rail operations themselves, but rather in the "connective tissue" that surrounds them. Drayage capacity, the trucking segment responsible for moving containers between rail ramps and final destinations, has notably tightened. J.B. Hunt explicitly flagged rising driver wages in its drayage operations as a cost headwind for its intermodal unit, indicating the pressure points within this crucial link of the supply chain. A shortage of drayage drivers or equipment can create bottlenecks, delaying the overall movement of freight even if rail lines are flowing efficiently.

Furthermore, transloading—the process of transferring goods from one type of container or mode of transport to another—remains a potential pinch point, particularly in markets experiencing uneven import flows. If imported goods arrive in volumes that overwhelm transloading facilities, it can create delays that ripple through the domestic intermodal network. The ability of the entire intermodal ecosystem—including railroads, drayage providers, and transloading facilities—to absorb this accelerated pace of conversion without experiencing service cracks that have derailed similar pushes in the past remains a critical question for the future.

Broader Market Implications and Future Outlook

The sustained surge in domestic intermodal volume carries significant implications for various stakeholders across the U.S. freight and logistics landscape.

For Shippers: The shift offers tangible cost savings, enhancing their ability to manage expenses in a challenging economic environment. It also provides a valuable alternative to a sometimes volatile truckload market, potentially improving supply chain resilience and predictability for long-haul freight.

For the Trucking Industry: While intermodal’s growth may pressure long-haul truckload rates, it could also allow trucking companies to reallocate assets to shorter-haul, higher-margin lanes, or to specialize in drayage services, which are integral to intermodal operations. The industry will need to adapt to this evolving competitive landscape.

For Intermodal Providers: Companies like J.B. Hunt are well-positioned to capitalize on this trend, gaining market share and potentially increasing profitability. The validation of their intermodal strategy, particularly in a period of such significant conversion activity, reinforces their long-term growth prospects.

For Class I Railroads: Increased intermodal volumes translate to higher revenue and better utilization of their extensive rail networks. However, it also necessitates ongoing investment in infrastructure, locomotives, and personnel to maintain service levels and prevent bottlenecks. Efficient intermodal operations are increasingly vital to their overall financial health.

For the Broader Economy: This trend can contribute to more efficient goods movement, potentially helping to mitigate inflationary pressures by reducing transportation costs for consumer goods and industrial components. It also reflects a dynamic and adapting supply chain responding to economic realities.

The current data strongly suggests that the freight is showing up on rail regardless of some existing operational challenges. The critical test will be whether the underlying infrastructure and human capital can scale efficiently to accommodate this new normal. The market is clearly signaling a preference for intermodal’s cost-efficiency, and how the industry responds to the associated capacity and service demands will define the trajectory of U.S. freight in the coming years.

About the Chart of the Week

The FreightWaves Chart of the Week is a regular feature that highlights an intriguing data point from SONAR, providing insights into the state of the freight markets. Each week, a Market Expert selects a chart from SONAR’s extensive database, offering commentary to help industry participants visualize and understand real-time freight market dynamics. These charts, along with their accompanying analyses, are archived on FreightWaves.com for future reference, serving as a valuable resource for market intelligence.

SONAR is a comprehensive platform that aggregates data from hundreds of sources, presenting it through intuitive charts and maps. It provides real-time commentary from freight market experts, addressing critical questions and trends within the industry. The FreightWaves data science and product teams continuously release new datasets and enhance the client experience to ensure SONAR remains at the forefront of freight market analytics. For those interested in exploring the capabilities of SONAR, a demo can be requested directly through the FreightWaves website.

Upcoming FreightWaves Events

FreightWaves continues to foster industry dialogue and knowledge sharing through a series of upcoming events designed to address critical topics and trends in freight and logistics.

Brokerage Compliance Symposium: Scheduled for October 26, 2026, the day before the F3 festival, this symposium will delve into every compliance issue faced by brokerage firms. Experts, including attorneys and operators, will navigate topics such as fraud exposure, carrier liability, FMCSA rules, cargo theft, and insurance gaps, defining best practices for an evolving industry. The event will take place at The Signal at Chattanooga Choo Choo in Chattanooga, TN.

F3 Awards Dinner: On the evening of October 26, 2026, preceding the main festival, the F3 Awards Dinner will honor leading companies in the freight technology sector. The FreightTech100 companies will be recognized, and the highly anticipated FreightTech 25 and Shipper of Choice winners will be revealed live. This exclusive event, featuring a cocktail reception, dinner, and live music, brings together 300 industry leaders in a purpose-built setting at The Signal at Chattanooga Choo Choo in Chattanooga, TN.

F3: Future of Freight Festival: Spanning October 27-28, 2026, this festival is a premier gathering for the freight industry. Attendees can expect industry-defining keynotes, rapid-fire technology demonstrations showcasing cutting-edge innovations, and unparalleled networking opportunities across various experiences in Chattanooga. The festival also incorporates the inaugural F3 Awards Dinner, where the FreightTech and Shipper of Choice winners will be unveiled, celebrating excellence and innovation in the sector. The event will be hosted at The Signal at Chattanooga Choo Choo in Chattanooga, TN.

{kind=link}