Amazon Bedrock AgentCore Payments Previewed for April 2026, Enabling Autonomous AI Agent Transactions

The landscape of artificial intelligence is poised for a significant transformation with the recent announcement that Amazon Bedrock AgentCore will preview its first managed payment capabilities in April 2026. This groundbreaking development is set to empower AI agents with the ability to autonomously access and pay for a wide array of digital resources, including APIs, Managed Cloud Provider (MCP) servers, web content, and even services from other AI agents. Built through a strategic partnership with industry leaders Coinbase and Stripe, this initiative aims to eliminate the complex and often "undifferentiated heavy lifting" associated with designing and maintaining bespoke systems for billing, credential management, and compliance within AI operations. This strategic move by Amazon Web Services (AWS) signals a profound shift towards truly self-sufficient and financially integrated AI systems, promising to unlock unprecedented levels of automation and innovation across various industries.

The Evolution of AI Agents and the Autonomy Imperative

AI agents represent a critical evolution in artificial intelligence, moving beyond single-task execution to systems capable of understanding complex goals, breaking them down into sub-tasks, and executing multi-step plans to achieve desired outcomes. These agents leverage large language models (LLMs) and other generative AI capabilities to reason, plan, and adapt, making them powerful tools for automation in diverse fields such as customer service, data analysis, software development, and scientific research. However, a significant barrier to their full autonomy has been the inability to seamlessly interact with external, paid services without human intervention.

Historically, for an AI agent to access a premium API for real-time data, utilize a specialized cloud server for heavy computation, or subscribe to specific web content, a human operator was typically required to manage the payment, credentials, and compliance aspects. This manual oversight introduced friction, slowed down operations, and limited the scalability and responsiveness of AI-driven workflows. The process of building customized systems to handle these financial interactions involved intricate development efforts, integrating with various payment gateways, managing sensitive credentials securely, and ensuring adherence to diverse regulatory standards—a burden AWS refers to as "undifferentiated heavy lifting." This problem has become increasingly pronounced as enterprises seek to deploy more sophisticated and interconnected AI agents, driving the demand for a robust, secure, and managed solution for autonomous transactions.

AWS Bedrock, since its introduction, has been instrumental in democratizing access to foundational models (FMs) from leading AI companies, offering a fully managed service that allows users to easily build and scale generative AI applications. The subsequent introduction of Bedrock Agents further enhanced this by enabling developers to create agents that can perform complex business tasks by orchestrating multiple FMs, calling external tools, and integrating with enterprise data sources. The missing piece, until now, was the ability for these agents to autonomously manage their financial interactions for external services, a gap that AgentCore payments is specifically designed to fill.

Unpacking Amazon Bedrock AgentCore Payments: A New Paradigm

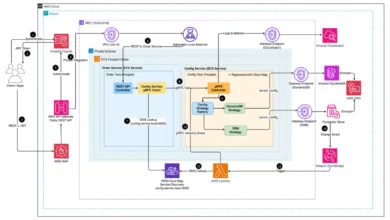

The core functionality of Amazon Bedrock AgentCore payments revolves around providing AI agents with managed capabilities to initiate and complete transactions for required external resources. This means that a sophisticated AI agent, designed to perform a research task, could, for instance, identify the need for real-time market data from a premium provider, autonomously connect to that provider’s API, pay for the data access, and integrate it into its ongoing analysis—all without human intervention in the payment process. Similarly, a coding agent could encounter a scenario requiring a specialized algorithm available only via a paid API, and AgentCore payments would facilitate the necessary transaction mid-task, ensuring uninterrupted workflow.

The technical integration leverages two prominent platforms for secure financial transactions: Coinbase CDP wallet and Stripe Privy wallet. Users can establish a payment connection by linking either of these wallets to their AgentCore setup. Coinbase, a leader in the cryptocurrency and digital asset space, provides a robust infrastructure for managing digital currencies, and its CDP (Coinbase Decentralized Protocol) wallet offers a secure, compliant pathway for institutional-grade digital asset transactions. This integration hints at future-proofing AI agents for interactions within the burgeoning Web3 economy, where decentralized applications and digital assets are becoming increasingly prevalent.

Stripe, renowned for its comprehensive suite of online payment processing tools and developer-friendly APIs, brings its expertise in traditional and emerging payment methods. The "Stripe Privy wallet" integration likely refers to a secure mechanism for managing credentials and initiating payments through Stripe’s extensive network, ensuring broad compatibility with various fiat payment methods and merchant services. By partnering with both Coinbase and Stripe, AWS provides a versatile and secure payment ecosystem that can cater to both traditional and digital asset-based transactions, offering flexibility and choice to developers.

A crucial aspect of AgentCore payments is the emphasis on governance and control through session-level spending limits. While enabling autonomy, AWS recognizes the paramount importance of preventing uncontrolled expenditures. Developers and enterprises can configure specific spending limits for each agent session, ensuring that financial transactions remain within predefined budgets. This feature is vital for risk management, compliance, and maintaining cost efficiency, providing a necessary safeguard against unintended financial outlays by autonomous agents. This balance between autonomy and control is fundamental to fostering trust and widespread adoption of financially enabled AI agents.

Strategic Alliances: Coinbase and Stripe Powering the Future of AI Finance

The selection of Coinbase and Stripe as foundational partners for AgentCore payments underscores a strategic vision by AWS to integrate established, secure, and scalable payment infrastructures into the AI ecosystem. These partnerships are not merely transactional; they represent a convergence of cloud computing, AI, and financial technology, paving the way for unprecedented capabilities.

Coinbase’s involvement brings a deep understanding of digital asset management, blockchain technology, and the evolving regulatory landscape surrounding cryptocurrencies. The Coinbase CDP wallet, designed for institutional clients, provides the secure and compliant rails necessary for AI agents to engage in transactions involving digital currencies or other tokenized assets. This partnership strategically positions AgentCore to interact with decentralized finance (DeFi) protocols and other Web3 services, expanding the potential scope of AI agent operations beyond traditional financial systems. For Coinbase, this represents an expansion of its platform’s utility, demonstrating its adaptability to new technological frontiers and its commitment to enabling enterprise-grade digital asset solutions within the AI domain.

Stripe’s participation is equally significant. As a global leader in online payment processing, Stripe offers a robust, developer-centric platform that handles billions of dollars in transactions annually. Its expertise in building scalable, secure, and user-friendly payment APIs is critical for ensuring that AgentCore payments are reliable and easy to integrate for a broad range of developers. The "Stripe Privy wallet" integration, likely leveraging Stripe’s secure credential management and payment initiation capabilities, ensures that AI agents can seamlessly interact with a vast network of merchants and service providers that accept traditional payment methods. For Stripe, this partnership solidifies its position at the forefront of innovation, adapting its core services to power the next generation of autonomous digital commerce and AI-driven economies.

Together, these partnerships address the multifaceted challenges of billing, credential management, and compliance. By abstracting these complexities, AWS allows developers to focus on building the intelligence and functionality of their AI agents, rather than expending resources on financial plumbing. This collaborative approach enhances security, ensures regulatory adherence, and provides a scalable foundation for the future of AI-driven transactions.

A Glimpse into the Future: The 2026 Preview and Beyond

The announcement of a preview for Amazon Bedrock AgentCore payments in April 2026 is a significant marker in the timeline of AI development. While it indicates a future release, the early preview announcement allows AWS to communicate its long-term strategic vision and gather feedback from early adopters, ensuring that the eventual general availability meets the evolving needs of the developer and enterprise communities. This forward-looking approach is characteristic of AWS’s strategy, often unveiling ambitious projects well in advance to set industry direction and foster innovation.

The broader timeline of AWS Bedrock began with its initial launch in April 2023, offering a fully managed service for FMs. This was followed by the introduction of agents for Bedrock, enabling multi-step task execution. The 2026 preview of AgentCore payments represents the next logical, and arguably most crucial, step towards achieving true end-to-end autonomy for AI agents. It signifies AWS’s commitment to building a comprehensive ecosystem where AI agents are not just intelligent but also capable of independently managing their operational costs and resource acquisition.

Looking beyond the 2026 preview, the roadmap for AgentCore payments likely includes expanding the range of supported payment connections, integrating with more diverse financial services, and enhancing governance features. As the technology matures, we can anticipate more sophisticated use cases emerging, potentially leading to fully autonomous AI entities that can operate, grow, and even generate revenue with minimal human intervention.

The Economic and Technological Landscape: Why This Matters Now

The timing of this announcement is particularly pertinent given the explosive growth of the AI and generative AI market. Reports from various industry analysts project the global generative AI market to reach hundreds of billions of dollars within the next decade, with enterprise adoption accelerating rapidly. Companies are increasingly investing in AI solutions to drive efficiency, foster innovation, and gain competitive advantages. However, the scalability and practical deployment of these solutions often hit bottlenecks when human oversight is consistently required for routine operational tasks, especially those involving financial transactions.

The "API economy" has also matured significantly, with a vast ecosystem of services accessible programmatically. From specialized data providers to sophisticated cloud functions, a wealth of resources can be leveraged by AI. AgentCore payments bridges the gap between the intelligence of AI agents and the economic realities of accessing these valuable resources. By enabling autonomous payments, AWS is effectively unlocking a new dimension of the API economy for AI, allowing agents to become active participants rather than passive consumers dependent on human intermediaries.

Furthermore, the demand for scalable, secure AI solutions that integrate seamlessly with existing enterprise financial systems is at an all-time high. Companies are grappling with how to deploy AI responsibly, ensuring cost control, security, and compliance. AgentCore payments directly addresses these concerns by offering a managed service that incorporates robust security protocols and the ability to set granular spending limits, thereby mitigating financial risks associated with autonomous AI operations. This development is set to accelerate enterprise AI adoption by providing a crucial piece of the puzzle for deploying truly intelligent, self-sufficient systems.

Industry Voices: Anticipation and Vision

While specific official statements regarding the 2026 preview were not provided in the original content, the implications allow for logical inferences about the perspectives of related parties.

AWS’s Vision: It can be inferred that AWS views AgentCore payments as a cornerstone for building the next generation of intelligent applications. An AWS spokesperson might emphasize how this service "removes the undifferentiated heavy lifting," allowing developers to "focus on innovation" rather than infrastructure. They would likely highlight the "seamless integration" with existing AWS services and the commitment to "security, compliance, and controlled autonomy" as foundational principles. The vision is likely centered on enabling customers to "build more powerful, cost-effective, and truly autonomous AI agents" that can "unlock new business models and operational efficiencies."

Coinbase’s Perspective: Coinbase would likely position this partnership as a testament to its platform’s security and its growing role in bridging traditional finance with the digital asset economy for institutional clients. A Coinbase representative might state that they are "thrilled to partner with AWS to empower AI agents with secure, compliant access to digital asset transactions," further emphasizing their commitment to "innovation in Web3 and the future of autonomous finance." They would likely underscore how the Coinbase CDP wallet provides "the trusted rails for AI agents to navigate the digital economy."

Stripe’s Contribution: Stripe would probably highlight its dedication to powering online commerce in all its forms, including the emerging "agent economy." A Stripe executive might comment on how this collaboration "extends Stripe’s mission to increase the GDP of the internet by enabling AI agents to transact seamlessly and securely." They would likely focus on the "developer-friendly nature" of their platform and how it provides "the robust infrastructure for AI agents to access a vast ecosystem of services."

Developer and Enterprise Reactions: The developer community is likely to express considerable excitement. Developers will anticipate streamlined workflows, reduced integration complexities, and the ability to create more sophisticated and impactful AI applications. Enterprises, on the other hand, would foresee significant gains in automation, operational efficiency, and the ability to leverage AI for tasks that were previously too complex or resource-intensive to fully automate. Concerns about security and cost control would be largely assuaged by the managed service approach and the implementation of spending limits, fostering greater confidence in deploying financially autonomous AI.

Broader Implications: Shaping the Autonomous Economy

The introduction of Amazon Bedrock AgentCore payments carries profound implications, signaling the dawn of a truly autonomous economy. For businesses, this means the potential for unprecedented operational efficiencies. AI agents could manage supply chains, optimize resource allocation, conduct market research, negotiate contracts, and even autonomously procure necessary services, dramatically reducing human intervention in repetitive or data-intensive tasks. This could lead to leaner operations, faster decision-making cycles, and a significant competitive advantage for early adopters.

The emergence of financially autonomous AI agents could also foster entirely new service models and AI-driven marketplaces. Imagine an ecosystem where specialized AI agents offer their services to other agents or human users, with transactions occurring seamlessly through AgentCore payments. This could create a dynamic "agent economy," where AI entities are not just tools but active participants in economic exchanges, potentially leading to new forms of value creation and distribution.

However, this paradigm shift also necessitates robust governance, ethical frameworks, and an evolving regulatory landscape. As AI agents gain financial agency, questions around accountability, liability, and ethical decision-making in financial contexts become paramount. The initial implementation of session-level spending limits is a crucial step in establishing control, but future iterations will likely require more sophisticated auditing capabilities, transparent transaction logs, and potentially regulatory oversight mechanisms to ensure responsible deployment. The industry will need to collaboratively address these challenges to build public trust and ensure that autonomous AI benefits society broadly.

Security and control mechanisms, therefore, will remain foundational elements. The partnerships with Coinbase and Stripe inherently bring a high level of financial security and compliance expertise. AWS’s commitment to enterprise-grade security within its cloud infrastructure further reinforces the trustworthiness of AgentCore payments. These measures are essential to prevent fraud, misuse, and unauthorized expenditures by autonomous agents, ensuring that the promise of intelligent autonomy is realized responsibly.

Engaging with the Future: Resources for Developers and Businesses

For developers and businesses eager to explore the potential of Amazon Bedrock AgentCore payments, AWS provides comprehensive resources. Interested parties can delve deeper into the capabilities by visiting the official blog post on machine learning, consulting the detailed documentation for technical specifications, and getting started with the AgentCore Command Line Interface (CLI) for practical implementation. These resources are designed to equip users with the knowledge and tools necessary to begin experimenting with and building the next generation of financially empowered AI agents.

Conclusion: Ushering in an Era of Intelligent Autonomy

The preview of Amazon Bedrock AgentCore payments for April 2026 marks a pivotal moment in the advancement of artificial intelligence. By enabling AI agents to autonomously manage their financial interactions for external services, AWS, in collaboration with Coinbase and Stripe, is removing a significant barrier to true AI autonomy. This development promises to unlock unprecedented levels of automation, foster new business models, and accelerate innovation across industries. While the full implications of financially autonomous AI agents will continue to unfold, this strategic move by AWS firmly establishes a foundation for an era of intelligent autonomy, where AI systems are not just smart, but also self-sufficient and seamlessly integrated into the global economy.

{kind=link}